Journal of Accountancy Reports Lower Auto Depreciation Limits for 2025

Martha Waggoner at the Journal of Accountancy published an analysis of Rev. Proc. 2025-16, the IRS guidance that sets depreciation limits for passenger automobiles placed in service during 2025. The headline finding is notable: for the first time in at least three years, these limits have decreased.

The reduction reflects stabilizing vehicle prices after years of inflation-driven increases. From 2021 to 2023, first-year limits jumped by $1,000 annually. That growth slowed to just $200 in 2024, and now the IRS has reversed course entirely.

For finance teams managing vehicle fleets as fixed assets, this shift carries practical implications. We track these annual updates closely because they directly affect depreciation schedules, tax planning, and asset record accuracy.

What the Numbers Look Like for 2025

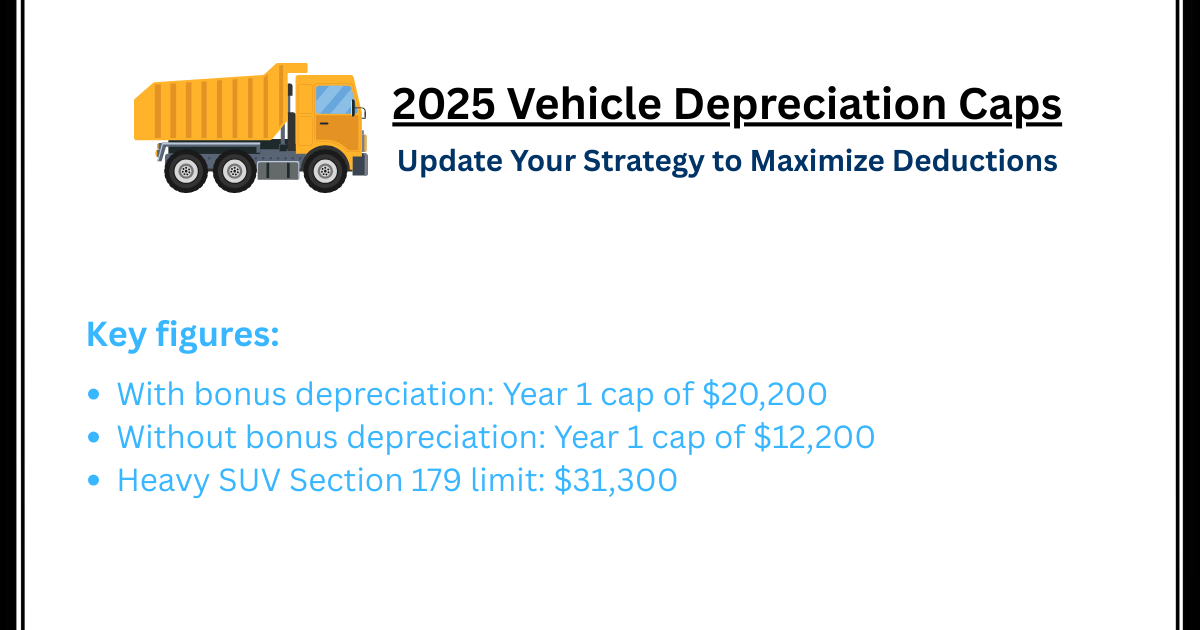

The Journal of Accountancy article details the specific Section 280F limits now in effect. These caps apply to passenger automobiles, which the IRS defines to include cars, trucks, and vans with a gross vehicle weight of 6,000 pounds or less.

For vehicles eligible for bonus depreciation:

• Year 1: $20,200 (down $200 from 2024)

• Year 2: $19,600 (down $200 from 2024)

• Year 3: $11,800 (down $100 from 2024)

• Year 4 and beyond: $7,060 (down $100 from 2024)

For vehicles without bonus depreciation, the first-year limit is $12,200, also $200 lower than 2024. The succeeding year limits mirror those above.

These reductions may seem modest in isolation. Across a fleet of 50 or 100 vehicles, however, the cumulative effect on first-year deductions becomes material.

Why the Limits Decreased This Year

The IRS adjusts these limits annually based on the automobile component of the Chained Consumer Price Index for Urban Consumers. When vehicle prices rise, limits increase. When prices stabilize or fall, limits can decrease.

According to Bureau of Labor Statistics data cited in the Journal of Accountancy article, used car and truck prices rose just 1% in the 12 months ending January 2025. New car prices actually dropped by 0.3% during that same period.

This price moderation contrasts sharply with 2021-2022, when supply chain disruptions and strong demand pushed vehicle prices sharply higher. The depreciation limits reflected that reality with consecutive $1,000 annual increases.

What This Means for Different Vehicle Types

Section 280F limits apply specifically to passenger automobiles as the IRS defines them. Understanding which vehicles fall under these caps helps finance teams plan effectively.

Vehicles subject to the 2025 caps:

- Passenger cars regardless of purchase price

- Light trucks and vans under 6,000 pounds gross vehicle weight

- SUVs under 6,000 pounds gross vehicle weight

Vehicles NOT subject to these caps:

- SUVs, trucks, and vans over 6,000 pounds gross vehicle weight

- Vehicles used for transporting persons or property for hire

- Ambulances, hearses, and certain specialty vehicles

For heavier vehicles exceeding the 6,000-pound threshold, different rules apply. These can qualify for more generous Section 179 expensing and bonus depreciation without the Section 280F caps.

Leased Vehicle Considerations

Rev. Proc. 2025-16 also updates the lease inclusion amounts for passenger automobiles first leased in 2025. These rules prevent lessees from circumventing the depreciation limits by leasing rather than purchasing.

When a leased vehicle's fair market value exceeds certain thresholds, the lessee must add an inclusion amount to gross income each year. This effectively reduces the lease deduction to approximate what depreciation deductions would have been under the ownership caps.

Finance teams managing mixed fleets of owned and leased vehicles need to track both sets of rules. The lease inclusion tables in the revenue procedure provide the specific dollar amounts based on fair market value ranges.

Planning Strategies for 2025 Vehicle Acquisitions

Lower depreciation limits extend the time required to fully depreciate passenger automobiles. For finance teams planning vehicle purchases, several strategies deserve consideration.

Consider vehicle weight carefully. Vehicles over 6,000 pounds gross vehicle weight are not subject to Section 280F limits. For businesses that can use larger vehicles, this threshold creates meaningful tax advantages.

Evaluate timing of acquisitions. The 2025 limits apply to vehicles placed in service during calendar year 2025. If your organization was planning significant fleet additions, understanding these lower caps helps set accurate expectations.

Document business use percentage accurately. The depreciation limits apply at 100% business use. When business use falls below 100%, the caps reduce proportionally. Accurate mileage logs and usage documentation support the deductions claimed.

Review Section 179 and bonus depreciation interaction. These provisions work together but remain subject to the Section 280F caps for passenger automobiles. First-year deductions cannot exceed the applicable limit regardless of which depreciation method applies.

How This Affects Fixed Asset Records

Vehicle depreciation limits change annually. Fixed asset systems need to accommodate these updates without disrupting existing records or creating calculation errors.

Key considerations for your asset register:

- Each vehicle should be tagged with its placed-in-service year to apply the correct limit table

- Depreciation schedules need the applicable caps built into calculations

- Bonus depreciation elections should be documented at the asset level

- Business use percentages require tracking when less than 100%

- Vehicles crossing the 6,000-pound threshold need different depreciation treatment

Spreadsheet-based tracking becomes increasingly difficult as depreciation rules add complexity. Purpose-built fixed asset software handles these annual updates systematically.

The Bottom Line for Finance Teams

The Journal of Accountancy coverage of Rev. Proc. 2025-16 highlights an important shift in vehicle depreciation rules. After years of increasing limits, the IRS has reduced caps across all recovery years for the first time since at least 2022.

For organizations managing vehicle fleets, these changes affect depreciation schedules, tax projections, and fixed asset records. The reductions are relatively modest, but they compound across multiple vehicles and multiple years.

Accurate fixed asset management requires staying current with these annual updates. Whether you track five vehicles or five hundred, applying the correct depreciation limits ensures compliant tax reporting and reliable financial records.

Frequently Asked Questions

What is the depreciation limit for vehicles in 2025?

For passenger automobiles placed in service in 2025 with bonus depreciation, the first-year limit is $20,200. Without bonus depreciation, the first-year limit is $12,200. These limits apply to cars, light trucks, and vans with a gross vehicle weight of 6,000 pounds or less.

What is the luxury car limit for depreciation?

The Section 280F "luxury auto" limits apply to all passenger automobiles regardless of actual price. For 2025, the caps are $20,200 (year 1 with bonus), $19,600 (year 2), $11,800 (year 3), and $7,060 (year 4 and beyond). These limits restrict depreciation deductions even for moderately priced vehicles.

What vehicles are not subject to Section 280F limits?

Vehicles with a gross vehicle weight rating over 6,000 pounds are exempt from Section 280F depreciation caps. This includes many full-size SUVs, pickup trucks, and cargo vans. Vehicles used for transporting persons or property for hire, ambulances, and hearses are also excluded.

Why did vehicle depreciation limits decrease in 2025?

The IRS adjusts depreciation limits annually based on vehicle price inflation. After years of sharp price increases, the automobile component of the Consumer Price Index moderated. Used vehicle prices rose only 1% and new car prices fell 0.3% in the 12 months ending January 2025, resulting in the first limit decrease in at least three years.

How does bonus depreciation work with the Section 280F limits?

Bonus depreciation provides an additional $8,000 first-year allowance for qualifying passenger automobiles. Combined with regular depreciation, this creates the $20,200 first-year cap for 2025. The bonus applies to vehicles acquired after September 27, 2017, and placed in service during 2025 with more than 50% business use.